IMPLEMENTATION EUROPEAN SUSTAINABILITY REPORTING STANDARDS

DOI:

https://doi.org/10.31617/3.2024(133)08Keywords:

reporting, sustainable development, reporting on sustainable development, non-financial reporting, integrated reporting, European sustainability reporting standards, standardization, corporate social responsibility, corporative management.Abstract

The introduction of European sustainability reporting standards into the process of corporate reporting can have a significant impact on the development of sustainable business and increase its social responsibility to society as a whole. The implementation of the requirements of the EU Directive 2022/2464 "On corporate sustainability reporting" into the general practice of reporting in Ukraine involves a detailed study of its requirements, as well as implementation into national legislation through standardization, clarification and the provision of methodological and methodical recommendations for the creation of corporate sustainability reporting. The purpose of the study is to identify the conceptual foundations of ESRS for the development of approaches to their implementation in the national practice of corporate reporting, which will allow the implementation of the requirements of EU Directive 2022/2464 in Ukraine. The general scientific and special methods were used: trend analysis, dialectical method, method of induction and deduction, analysis, synthesis, method of concretization, generalization, systematization, visualization, hypothetical method and bibliometric analysis. The study is designed to improve the theoretical and methodological provisions regarding the implementation of ESRS in Ukraine by developing an authorʼs approach to their implementation. This made it possible to develop the basis for the introduction of European reporting standards on sustainable development into the national reporting practice. In the article a three-stage approach to determining essential information about risks and opportunities associated with sustainable development was characterized; the composition of the European sustainability reporting standards was analysed and their characteristics were provided; the stages of application of European sustainability reporting standards in the countries of the European Union were investigated; the advantages and disadvantages of reporting on sustainable development based on European sustainability reporting standards were analysed; a matrix of the ratio of European sustainability reporting standards to other regulations in the field of reporting on sustainable development has been developed; approaches for further implementation of ESRS in the national practice of reporting in Ukraine have been proposed.

References

About COP28. (2023). https://www.cop28.com/en/about-cop28

Al-Nawaiseh, H. N., Nawaiseh, M. E., Bader, A., Mubaset, Z. & Adel, A. (2023). Sustainability Reporting Adoption in Jordanian Listed Firms: Does Corporate Social Responsibility Matter? Studies in Big Data, (Vol. 136), (pp. 56-70). https://doi.org/10.1007/978-3-031-42455-7_6

Annex 1 to the Commission Delegated Regulation supplementing Directive 2013/34/EU as regards sustain-ability reporting standards. (2023). http://ec.europa.eu/finance/docs/level-2-measures/csrd-delegated-act-2023-5303-annex-1_en.pdf

Annex 2 to the Commission Delegated Regulation supplementing Directive 2013/34/EU as regards sustain-ability reporting standards. (2023). http://ec.europa.eu/finance/docs/level-2-measures/csrd-delegated-act-2023-5303-annex-2_en.pdf

Barker, R. (2024). Get Ready for More Transparent Sustainability Reporting. MIT Sloan Management Review, 65(2), pp. 34-37.

Das, S. K., Khalilur Rahman, M., & Roy, S. (2024). Does ownership type affect sustainability reporting disclosure? Evidence from an emerging market. International Journal of Disclosure and Governance, 21(1), 52-68. https://doi.org/10.1057/s41310-023-00180-w

de Villiers, C., Dimes, R., & Molinari, M. (2024). How will AI text generation and processing impact sustainability reporting? Critical analysis, a conceptual framework and avenues for future research. Sustainability Accounting, Management and Policy Journal, 15(1), 96-118. https://doi.org/10.1108/SAMPJ-02-2023-0097

Dinh, T., Husmann, A. & Melloni, G. (2023). Corporate Sustainability Reporting in Europe: A Scoping Review. Accounting in Europe, (Vol. 20(1), (pp. 91-119). https://doi.org/10.1080/17449480.2022.2149345

Directive (EU) 2022/2464 of the European Parliament and of the Council of 14 December 2022 amending Regulation (EU) No 537/2014, Directive 2004/109/EC, Directive 2006/43/EC and Directive 2013/34/EU, as regards corporate sustainability reporting. https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32022L2464

Ebaid, I. E.-S. (2023). Nexus between sustainability reporting and corporate financial performance: evidence from an emerging market. International Journal of Law and Management, (Vol. 65(2), (pp. 152-171). https://doi.org/10.1108/IJLMA-03-2022-0073

Förster, P. (2023). The Double Materiality Principle (Article 19a NFRD) as Proposed by the Corporate Sustainability Reporting Directive: An Effective Concept to Tackle Green Washing? European Yearbook of International Economic Law, (Vol. 13), (pp. 345-364). https://doi.org/10.1007/8165_2022_90

Giner, B. & Luque-Vílchez, M. (2022). A commentary on the "new" institutional actors in sustainability reporting standard-setting: a European perspective. Sustainability Accounting, Management and Policy Journal, (Vol. 13(6), (pp. 1284-1309). https://doi.org/10.1108/SAMPJ-06-2021-0222

Google Trends. (2023). https://trends.google.com/trends/explore?date=all&q=ESRS,SFDR,TCFD,ISBB,TNFD&hl=en

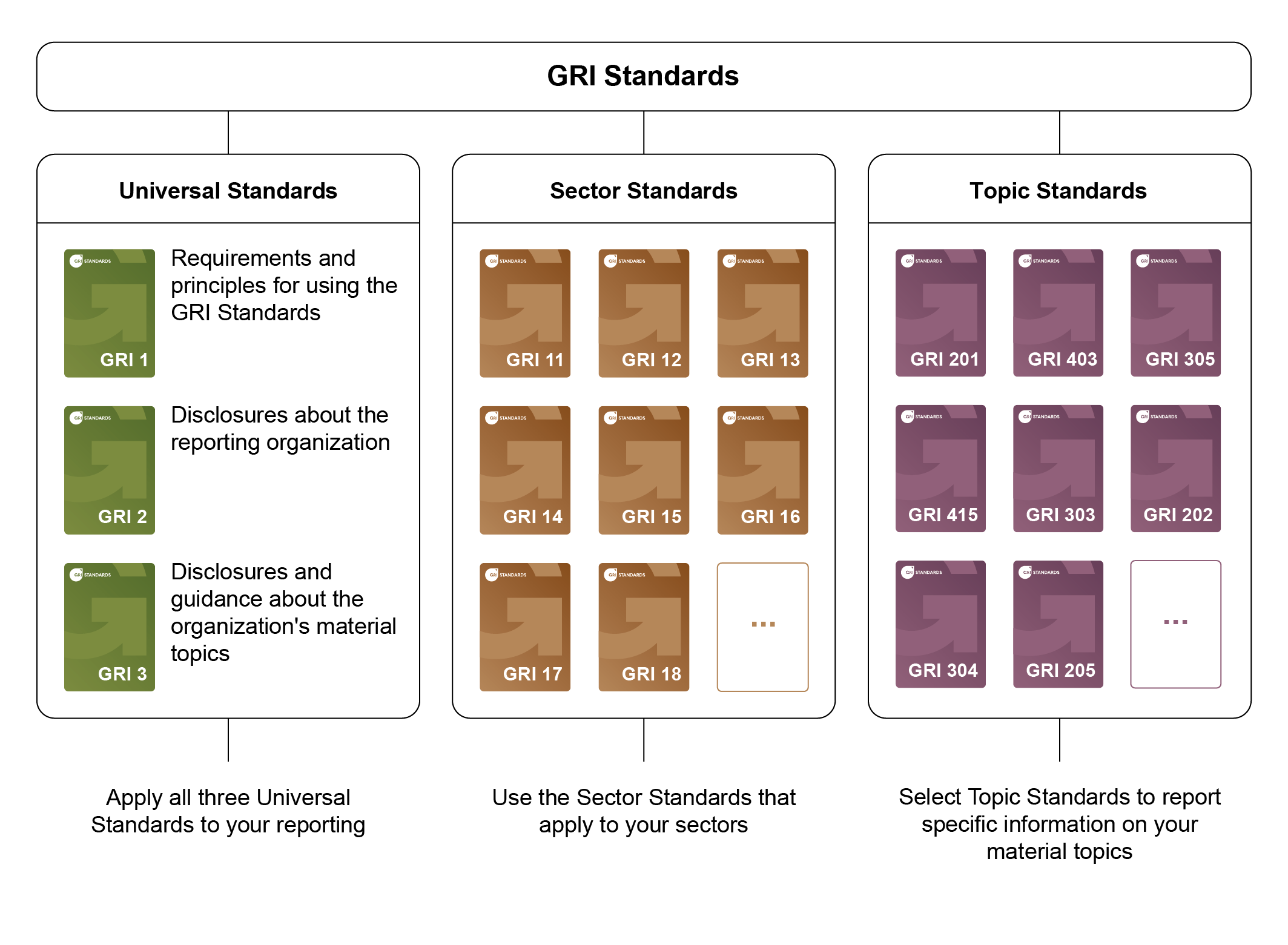

GRI Standards. (2021). https://www.globalreporting.org/media/s4cp0oth/gri-gristandards-visuals-fig1_family-2021-print-v19-01.png

Hardiningsih, P., Nuswandari, C., Srimindarti, C., Lisiantara, G. A., & Setiawati, I. (2024). A literacy of the relevance of Asian value sustainability reporting in Indonesia. Investment Management and Financial Innovations, 21(1), 76-87. https://doi.org/10.21511/imfi.21(1).2024.07

Hummel, K., & Jobst, D. (2024). An Overview of Corporate Sustainability Reporting Legislation in the European Union. Accounting in Europe. https://doi.org/10.1080/17449480.2024.2312145

Kwarto, F., Nurafiah, N., Suharman, H., Dahlan, M. (2024). The potential bias for sustainability reporting of global upstream oil and gas companies: a systematic literature review of the evidence. Management Review Quarterly, 74(1), 35-64. https://doi.org/10.1007/s11301-022-00292-7

Mahmood, Z., Blaber, Z. N., & Khan, M. (2024). Institutionalisation of sustainability reporting in Pakistan: the role of field-configuring events and situational context. Qualitative Research in Accounting and Management. https://doi.org/10.1108/QRAM-01-2022-0019

Metelytsia, V. (2023). Sustainability reporting standardi-zation as a prerequisite for green post-war reconstruction of the agricultural sector, Sustainable Development of Economy, (Vol. 47, Iss. 2), (pp. 137-145). https://doi.org/10.32782/2308-1988/2023-47-20

Monteiro, S., Guzmán, B. A. & García Sánchez, I.-M. (2023). The role of sustainability reporting in corporate tax transparency. Taking on Climate Change Through Green Taxation, (pp. 318-334). https://doi.org/10.4018/978-1-6684-8592-7.ch014

Nõmmela, K. & Kõrbe Kaare, K. (2022). Incorporated Maritime Policy Concept: Adopting ESRS Principles to Support Maritime Sectorʼs Sustainable Growth. Sustainability (Switzerland), (Vol. 14(20), 13593. https://doi.org/10.3390/su142013593

Pasko, O., Balla, I., Levytska, I., & Semenyshena, N. (2021). Accountability on Sustainability in Central and Eastern Europe: An Empirical Assessment of Sustainability-Related Assurance. Comparative Economic Research. Central and Eastern Europe, 24(3), 27-52. https://doi.org/10.18778/1508-2008.24.20

Pigatto, G., Cinquini, L., Dumay, J., & Tenucci, A. (2023). A critical reflection on voluntary corporate non-financial and sustainability reporting and disclosure: lessons learnt from two case studies on integrated reporting. Journal of Accounting and Organizational Change, (Vol. 19(2), (pp. 250-278). https://doi.org/10.1108/JAOC-03-2022-0055

Pizzi, S., Caputo, F., de Nuccio, E. (2024). Do sustainability reporting standards affect analystsʼ forecast accuracy? Sustainability Accounting, Management and Policy Journal, 15(2), 330-354. https://doi.org/10.1108/SAMPJ-04-2023-0227

Sustainability reporting key to profitability and success, says new guide from ACCA. (2023). https://www.accaglobal.com/gb/en/news/2023/november/sustainability-reporting-guide.html

Sustainability reporting - the guide to preparation. (2023). https://www.accaglobal.com/content/dam/ACCA_Global/professional-insights/sustainability-reporting/PI-SUSTAINABILITY-REPORTING-THE-GUIDE-TO-PREPARATION.pdf

The International Framework (2022). http://www.integratedreporting.org/wp-content/uploads/2022/08/IntegratedReportingFramework_081922.pdf

Ukraine 2023 Report. (2023). https://neighbourhood-enlargement.ec.europa.eu/system/files/2023-11/SWD_2023_699%20Ukraine%20report.pdf

Vitols, S. (2023). The emerging corporate sustainability reporting system: what role for workersʼ represen-tatives? Transfer: European Review of Labour and Research, (Vol. 29(2), (pp. 261-265). https://doi.org/10.1177/10242589231175607

Waas, B. (2023). Some thoughts on the new EU-directive on corporate sustainability reporting. Zbornik Pravnog Fakulteta u Zagrebu, (Vol. 73(2-3), (pp. 457-473). https://doi.org/10.3935/zpfz.73.23.11

Whittingham, K. L., Earle, A. G., Leyva-de la Hiz, D. I. & Argiolas, A. (2023). The impact of the United Nations Sustainable Development Goals on corporate sustainability reporting. BRQ Business Research Quarterly, (Vol. 26(1), (pp. 45-61). https://doi.org/10.1177/23409444221085585

Xie, J., Tanaka, Y., Keeley, A. R., Fujii, H. & Managi, S. (2023). Do investors incorporate financial materiality? Remapping the environmental information in corporate sustainability reporting. Corporate Social Responsibility and Environmental Management, (Vol. 30(6), (pp. 2924-2952). https://doi.org/10.1002/csr.2524

Korol, S. Ya., Semenova, S. M. & Courbet, M. A. (2022). Implementation of reporting on sustainable development in Ukraine: state and prospects in the context of European integration, Business-inform, (Vol. 1), (pp. 294-301). https://doi.org/10.32983/2222-4459-2022-1-294-301

Additional Files

Published

How to Cite

Issue

Section

License

This work is licensed under a Creative Commons Attribution 4.0 International License.

This work is licensed under a Creative Commons Attribution 4.0 International (CC BY 4.0)

{kind=link}